|

||

|

|

||

Moving Planner![]() Exit Tax Could Affect your Expatriation

Exit Tax Could Affect your Expatriation

By Barron Harper

www.taxbarron.com

US citizens and deemed residents (i.e. Green Card holders) are required annually to file a Federal Income Tax Return on which they are obliged to report their world-wide income flows. For those residing within the continental United States, the filing requirements are fairly standard with penalties being accessed for late filing and/or late payment. Although the Internal Revenue Service promotes the concept of ‘voluntary compliance’ as the American system of tax reporting, the flow of documents to the Service from payers of various income flows ranging from wages, nonemployee compensation, interest, dividends, sales of property and the like exposes this propaganda. Rather voluntary compliance is more correctly mandated and enforced by the threat of forms of punishment. But while Americans stateside may occasionally complain against the tax system, most readily comply in the knowledge that their tax dollars sustain systems of education, police and fire protection, road systems and so forth.

However the citizen-based taxation imposed on Americans abroad by contrast appear menacing and unbeneficial. To the basic tax return must often be added forms for Foreign Earned Income Exclusion (2555), Foreign Tax Credit (1116), Specified Foreign Holdings (8938), Passive Investments (8621), Foreign Corporations (5471), Foreign Partnerships (8865), Foreign Trusts (3520), Transfers to Foreign Corporation (926), and Foreign Banking Account Report (TD F 90-22.1). Failure to file these often complex forms carries stiff confiscatory penalties ranging from 5 – 50% of foreign investments plus criminal prosecution.

According to the late Vernon Jacobs (www.offshorepress.com): ‘The Internal Revenue Code contains more than 3.4 million words; printed 60 lines to the page, it would fill more than 7,500 letter size pages. To conserve space, the tax code uses extensive cross-referencing to other parts of the tax code as a substitute for explaining the cross reference in any semblance of English. This forces readers to look up numerous other parts of the tax code in order to understand the scope of any section with cross references. In spite of this mountain of verbiage, every citizen is presumed to be familiar with the entire US Tax Code.’

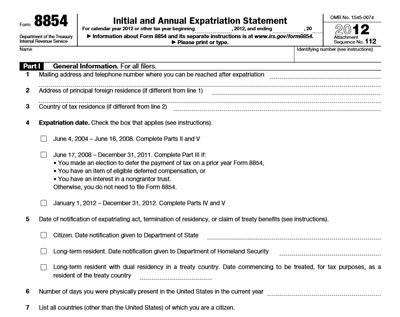

As increasing numbers of Americans, frustrated with the heavy-handed and confusing tax compliance mandates of the IRS, opt out of the system by rejecting their US citizenship (http://world.time.com/2013/01/31/mister-taxman-why-some-americans-working-abroad-are-ditching-their-citizenships/), the question of procedure emerges. Under the Heroes Earnings Assistance and Relief Tax Act passed in 2008, an exit tax is imposed on any ‘covered expatriate’: a US citizen who relinquishes citizenship or a long term resident who terminates permanent residency status after holding it for 8 out of the last 15 years, and who 1) had an average annual income tax liability of more than $151,000 (2012) for the preceding 5 years, 2) had a net worth of $2,000,000 in worldwide assets, and 3) failed under penalty of perjury to have complied with all federal tax obligations for the last 5 years. If the exit tax does not apply because items 1) and 2) do not qualify, the covered expatriate must under penalty of perjury sign a statement that he/she complied with tax obligations for the last 5 years, and file Form 8854 and a final tax return.

If the exit tax applies, the covered expatriate pays the tax on any unrealized gains above $651,000 (2012) according to mark-to-market taxation as though the property or properties worldwide were sold on the day before expatriation. The resulting gains less unrealized losses are added to any other taxable income of the expatriate’s last year in the United States. If adequate security is provided, any resulting tax liability can be deferred until the year the property is sold at an interest rate applicable to underpayments of tax. But if the tax is deferred, Form 8854 must be filed annually up to and including the year in which the full amount of deferred tax and interest is paid. The expatriate must also waive any right under any US tax treaty that would preclude the assessment or collection of the tax. As the tax code does not provide for any foreign tax credit on income taxes paid to a foreign country on property sales within that country’s jurisdiction, double taxation issues will have to be clarified.

Any deferred compensation items will also be included in income and taxed at US income tax rates or else subject to 30% withholding tax when later paid out to the expatriate. Included items are eligible deferred accounts such as IRA, health savings account, qualified tuition plan, or Archer Medical Savings Account. 30% items would be qualified tuition plan, stock bonus or profit sharing plans, (401(k)’s and interest in foreign pension plan.

Any covered gifts or bequests of the expatriate to a US citizen or resident in excess of $14,000 ($143,000 to noncitizen spouse) will be taxed to the recipient at 35% or the highest gift tax rate in effect (spouses excepted) in the year of transfer. Property in a grantor trust in which the covered expatriate is the grantor is also subject to the exit tax.

Note that an individual continues to be treated as a US citizen or long term resident (LTR) for US tax purposes until he/she 1) gives notice of an expatriating act or termination of residency to the Secretary of State or Secretary of Homeland Security, and 2) provides a statement to the Secretary of the Treasury in accordance with IRC Section 6039G. Once citizenship is relinquished on the earliest of four possible dates – 1) the date the individual renounces US nationality before a diplomatic or consular officer of the United States (provided that the voluntary relinquishment is later confirmed by the issuance of a certificate of loss of nationality), 2) the date on which the individual furnishes to the State Department a signed statement of voluntary relinquishment of US nationality confirming the performance of an expatriating act, 3) the date that the State Department issues a certificate of loss of nationality, 4) the date that a US court cancels a naturalized citizen’s certificate of naturalization – US citizenship or LTR treatment ceases. Relinquishment can also occur under Treasury regulations with respect to an individual who became at birth a citizen of the United States and of another country.

Coincidentally Form 8854 must then be filed with the expatriating filer’s individual income tax return. This detailed and complex form requires that the taxpayer report his/her Taxpayer Identification Number, mailing address of principal foreign residence, foreign country of residence and citizenship, detailed information of income, assets and liabilities, number of days physically present in the United States, and such other information as the Secretary may prescribe. Naturally there is a penalty for failing to file this form: $10,000.

In today’s complex world, keeping what some will perceive as a predatory tax authority at bay will require taking steps to understand the process of expatriation, determining covered expatriate status, filing any back tax and information returns, applying for the Loss of Naturalization from the Department of State, and filing Forms 1040 or 1040NR and 8854 with the Internal Revenue Service Center at Philadelphia, PA 19255-0549.

Conclusion

My dad’s father was a central Missouri hill country farmer and rancher. He was a man of absolute integrity on whose word you could depend under any circumstance. In the early 1960s when he was 71 years of age, he lamented that a kind of golden era had passed in which Americans could conduct business on a handshake. Thirty years later Francis Fukuyama in his book Trust highlighted this American phenomenon in which he linked American prosperity to the establishment of Social Capital; this he defined as people trusting each other across the continent to fulfill commitments. After World War II this Social Capital has been in decline with the emergence of antagonizing systems of costly control replacing human integrity in social dealings. The result is fragmentation when in reality cohesion is what advances Social Capital.

|

Sign-up for the FREE Americans in France newsletter! |

cookieassistant.com